Years Until Retirement

Amount to Invest Today $

Amount at Retirement in Today's Dollars:

Amount to Invest Today $

Amount at Retirement in Today's Dollars:

The investing strategy that I follow is a “get rich slowly” scheme. I’m not into chasing down returns. I don’t need high risk/high reward for the majority of my investments. If you don’t want to spend your life consumed by what the stock market is doing, keep reading. If you feel like that is something you need, I recommend pulling out 5% of your portfolio and doing day trading or cryptos or whatever you need to do to get that out of your system, because emotion based investing is the enemy of your portfolio. I understand that for some people there is relational component; that picking stocks or sharing in current trends may allow you to participate in conversations with your friends. I don’t discount that, but if you want the best returns on average, with significantly lower risk overall, don’t do that with your main portfolio.

I could have titled this post “Investing Strategies for Boring People”, but you probably wouldn’t have clicked on that one would you? If you like high risk activities, and want your money to make a huge gains, find another website. What I’m espousing here will change your life, and leave you with a near 100% certainty of adequate nest egg upon retirement, but it won’t double your initial investment in 6 months. That kind of growth is unsustainable, and certain to reverse at some point. The risk is commensurate with the reward.

Some people hear the term “Passive Investment” and think bad returns. That is simply not the case. I like investing in the entire stock market. The real return of the market is 8.8 percent since 1887 (that is without the negative annual return of 2% from inflation, so actual rate would be 6.8%). That is a rate of return that would allow you to retire comfortably on just 6k per year investment throughout your working life.

Passive investment should be part of your investment strategy, if you get the itch to actively invest (I accept that people like to gambling with their money for fun) it is highly expedient for your long term wealth building that you only do so with a small part of your portfolio. The risk from this method is that you may not even get the baseline of the total stock market’s annual increase, additionally, you are likely exposing yourself to several times the amount of risk, so your risk adjusted return was even lower! Risk is one of the most underestimated factors in any investment strategy. When you invest in a high risk sector, you basically become your own insurance. If a catastrophic event occurs, you are the one who pays out, if no catastrophic event occurs, you make money, and good money at that! Ever read the “Black Swan” by Nassim Taleb? There are always unforeseen catastrophic negative events that will occur. So beware.

I’ve noticed that whenever stocks are going up more rapidly then normal, the stock market tends to a get a lot of additional press attention, and this often draws inexperienced investors into the market at the worst possible time to enter the market. When the market corrects there is a lot of negative press, and inexperienced investors may be influenced by these reports to get out of the market. Fight that urge.

This is what happens when you try to beat the market average. People trying to beat the market find themselves on the losing side just as often as the winning side, but they pay a higher price. The fees of an actively managed account often eat up the profit that the account claims to deliver. In addition to this, the tax implications from all the trades necessary in an actively managed account make it a particularly poor choice for non-tax advantaged accounts. It is estimated that the global financial services market is 26.5 Trillion dollars. That’s Trillion with a T. 20-25% of the world economy. Someone is making money off of every dollar you save, invest, transfer, or send. It is in their best interest to convince you to pursue an actively managed account.

One of the largest indicators for the success of a fund is the expense ratio, it is pretty much the only thing that you know ahead of time when you buy into a fund. In the field of investing, it is a generally accepted maxim that “past performance is no guarantee of future results”.

Time to get practical:

The best place that you can dump your money if you want a “set it and forget it” approach to investing is a target retirement date fund from Vanguard such as VFFVX.

I’m a huge fan of Vanguard. They are non-profit, which allows them to have low fees on most/all of their mutual fund offerings, the funds I’ve used are:

Fidelity has some zero fee funds covering the U.S. and international stock markets. The funds are: FZROX and FZILX, and if I was just starting out and around 20-25, I’d consider dumping half in each.

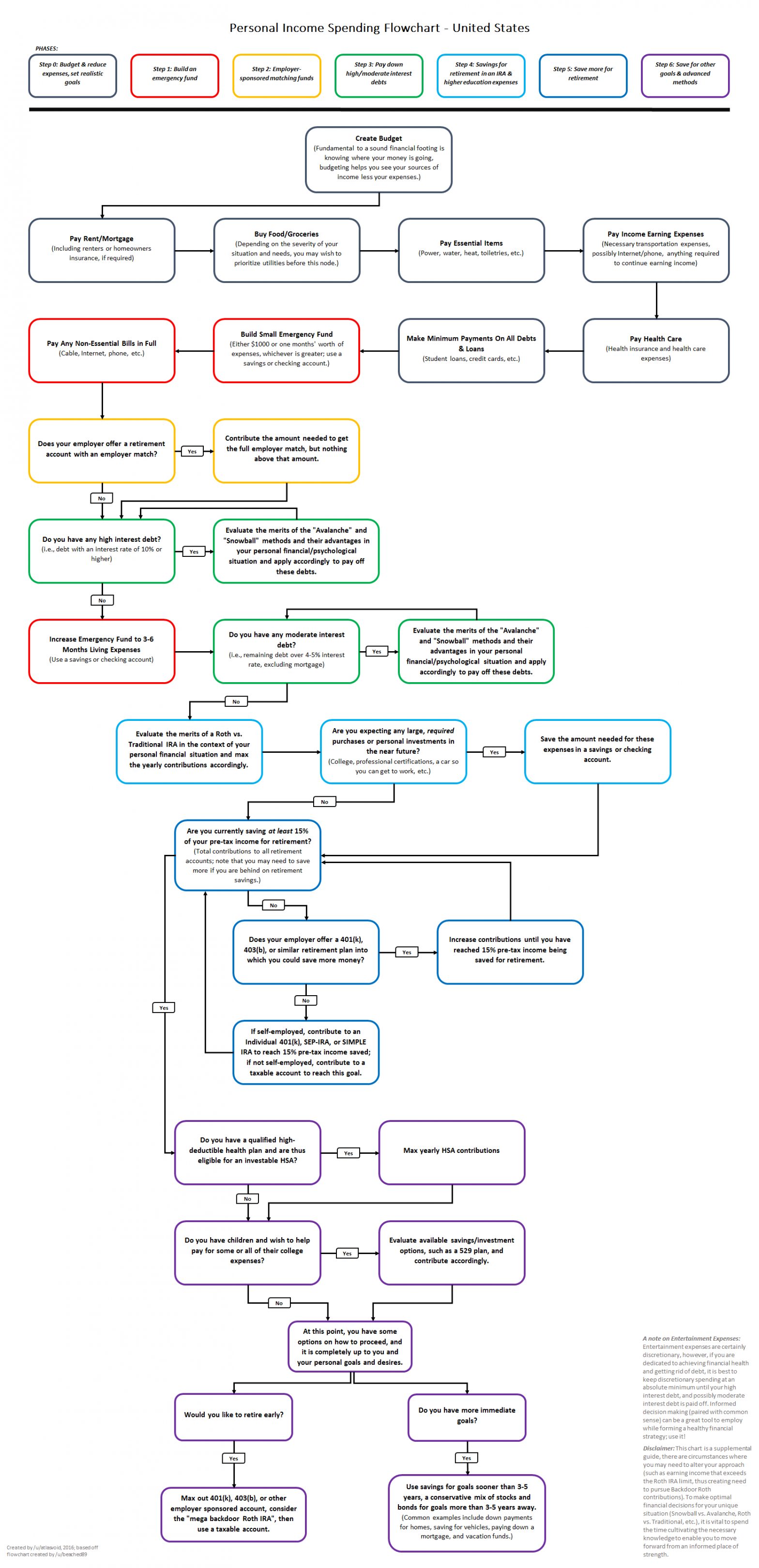

Please take the time to read the common topics section from Reddit’s “Personal Finance” website. That resource will give you a great overview of investing and personal finance. The graphical flowchart is an especially great resource.

I do not recommend investing if your timeline is less than 5 years (as would be the case if you were planning to pay off student debt with the money/put a down payment on a house/buy a car). In that case you’d want to consider a high interest Savings account or similar.

This will require you thinking ahead. It takes some serious planning in order to figure out what your future holds and what you will want to do with the money. Don’t hear me wrong, I think you should invest a percentage of every single paycheck that you earn over your career, but don’t plan to take any of that invested money out to finance a particular purchase in the near future.

There are other ways to invest intelligently besides the stock market. The ones that come to mind are Real Estate, Business Debt, and personal improvement(usually education). Please see my other articles on these subjects.

Don’t chase past earnings in mutual funds, and don’t pick stocks. You will not win in the long term. Everyone likes to remember (or brag about) that one pick from years ago that turned into an Amazon, but think of how many companies didn’t make it through the dot-com crash. Thousands… are you going to pick the stock that goes to the top? Unlikely. If there is any doubt about this point, I can forward you some literature so that you can convince yourself it is a bad idea to play with this. It is also a royal time-suck. Devote your time to getting better at your job or developing a sidehustle, not this.

One last site: firecalc.com

If firecalc doesn’t change your life, nothing will. It takes a minute to figure out how to use it, but it is fun to see what your investment will grow into if you let it.

https://www.citi.com/credit-cards/credit-card-details/citi.action?ID=citi-secured-credit-card

For those who are just starting their financial journey with no credit history, I recommend a secured card because most likely you will be turned down for anything else. Having a credit score is important because it allows you to use credit cards with rewards. (My credit card (Citi Double Cash) gives me 2% back on all purchases). It is also important if you decide to purchase a house anytime in the next 10 years or so. If you get turned down by one bank for a secured card, apply for another, and keep applying until someone is willing to take a chance on you. I walked into a US Bank at the age of 19, and was turned down by their system, but the banker called me a couple days later and said he was willing to take a chance on me. They made the right choice, as I’ve continuously maintained an account with them since then, and have yet to make a single late payment.

I recommend storing any savings that you will not be using in the next 4 months in this bank account: https://www.ally.com/?context=bank This bank gives you one of the higher % interest return per year for using them, as compared to 0.1% as an average for all banks in the US. This is important because it gives you a decent return with no effort on your part. It is dead simple to transfer money to and from your local bank’s checking account (or credit union) directly from this account. It literally takes 3 button clicks once you log in to transfer money either direction (And takes 1 business day).

For a retirement investment account, I recommend Vanguard: https://investor.vanguard.com/ira/iras

Create a Roth IRA and contribute up to $6000 (Your spouse or significant other can also contribute this much). This is taxed money, but it is not taxed when you pull it out at retirement, and you can also pull out what you put in at any time and with no penalties or fees. The fund that you will buy is a “Target Retirement Date fund” for year ~when you will retire. This manages your funds for you so you never have to think about it. If you want to invest more than this, or in other things, you can, but I’d recommend this at a minimum every year you are working.

“Investors should remember that excitement and expenses are their enemies. And if they insist on trying to time their participation in equities, they should try to be fearful when others are greedy and greedy only when others are fearful.” — Warren Buffett

There is money to be made on the meteoric rise of cryptocurrencies, just watch out that you don’t lose it all on the way back down. Like every bubble, there will be winners and there will be losers.

Like any investment strategy, the potential reward for investment must balance out the risk. At this stage, Cryptocurrencies are both risky and (potentially) very rewarding. Anytime there is “easy money” to be made, there is going to be an eventual collapse, because when the people that flocked to an investment due to a sharp increase in price experience their first dramatic decrease in price, they won’t enjoy it, and will pull out of the market, or switch to another investing medium. “But,” you exclaim “retail investors only account for 20% of the market!”. That is indeed true, but there are two things you need to remember:

You probably wouldn’t have guessed it, but I’m actually very bullish on the role that cryptocurrencies will play in the future of mankind. What I’m not bullish about is any particular cryptocurrency. Do you remember the dot-com bust? Remember pets.com? No? It lasted 9 months after it’s IPO. I’m not saying that cryptocurrencies are stocks, they aren’t. What I’m saying is that survival of the fittest dictates that many die out before we find who will provide long term value to users, and eventually long term gain to investors.

I entered the cryptocurrency world with money that would have otherwise been left sitting in a bank account in late 2017. I didn’t bet big, because I was a poor college student. But I did it right, I had a well diversified portfolio of over 40 “alt-coins”. I realized at some point that the current market trajectory was unsustainable, (January 15th of 2018) and took my money out. For those who are wondering what happened in the market, the following 3 months were an absolute blood bath, it tanked, and tanked hard. I only took out what I had put in. I liked to pretend that the rest was “monopoly money” but in reality I still wanted to bet on the crypto currency market. In all I’ve roughly quintupled my initial investment. Am I happy about that? I guess I am, but I can’t help thinking that it was mostly luck. I had no idea what direction the market was going to go, and I had no idea when I needed to pull out of the market, I had no idea that if I left my money in there that the market would eventually come roaring back. I have a lot of friends that jumped in during that time, lost a bunch of money, sold out, and never got any of it back.

I learned a few different things about cryptocurrencies:

To date, I’ve although I’ve had many enthusiastic conversations about the technology behind cryptocurrencies, I have not yet counseled someone to buy, and I always tell people to sell. Don’t get me wrong, I’m bullish on the crypto-market in the long term, but I’m not bullish on the average individual being able to pick the winning cryptocurrency. So if you feel some urge to gamble 5% of your investment portfolio on something with serious upside….sure, go for the broad crypto market. Otherwise, stay far away.

For those who are interested in some further reading, allow me to point you to the following link… I’ll warn you that although there are plenty of coherent thoughts in this article on the crypto space, I don’t agree with him that there are zero potential use cases for Crypto, simply that the exuberance seen right now in the crypto market is severely misplaced and is in essence a massive bubble. I especially appreciate what he has to say about NFTs. https://www.currentaffairs.org/2022/05/why-this-computer-scientist-says-all-cryptocurrency-should-die-in-a-fire/