Alright, the last blog post got too long, so I decided to create another one so that I could add some more thoughts and to make it a manageable read.

A Bank Account

Banks make your money safer: The banks carry deposit insurance from the FDIC. All sorts of things can happen to money you store at your house: You could lose it, your house could burn down, someone could steal it, etc etc. If it is in an insured bank, you aren’t exposing yourself to those risks.

Banks pay you interest: Additionally, a bit of interest will be added to your account (rates very widely bank to bank, so shop around). I use an online bank bank in conjunction with a local Credit Union.

Banks also make your money a bit harder to get: Some people will argue that this makes no difference, but I’ve often had to pass up purchases that I later would of regretted simply due to not wanting to make a run to the bank. It might not work for you, but I know it has worked for me.

As a side note, bank accounts also are generally required to open an investment account, which is very important for your long term financial help.

Credit Cards

Credit cards. I am all for them. In fact, this year alone I’ve gotten $1100 in cash back & rewards from my credit cards. When you hit adulthood and you open a credit card, you need to make a rule for yourself that if you are ever forced to carry a balance from month to month, you will rip up that credit card and never reopen it. The benefits of having a credit card are nullified if it allows you to spend more than you otherwise would.

Don’t Spend Money On Things Bad For Your Body

Make it your rule to never buy something that you know is bad for you: Tobacco Products/drugs/alcohol obviously, but less obviously: soft drinks/candy/icecream.

Ask yourself…. Is it good for me? If the answer is yes, then it is a permissible expense. If the answer is no, then don’t buy it.

Financial wellness is a way of life. Just like physical wellness or mental health. These things don’t happen overnight, and they aren’t necessarily easy. But don’t be discouraged with temporary setbacks. Just keep taking steps in the right direction.

Subscriptions

Subscriptions are the devil. There is a reason that all the major software and media businesses are moving to a subscription model. Let me give you a hint, it isn’t so that they can charge you less money over time. Nothing kills your budget faster than guaranteed monthly expenses. The average American spends over $200 monthly on subscriptions. Your goal for subscriptions should be that you spend zero dollars on them. See my post on subscriptions.

Phone Plans

If you are spending more than $35 on a phone plan, you are being robbed. I spend less than $20 a month for 10gb of non-deprioritized data on the AT&T network with unlimited talk & text (Red Pocket for those of you wondering what plan I’m on)

Cheap Cars

I found that cars around the 130,000 mile mark, if they’ve been well maintained, will drive on into the mid-term future without issue. Usually these cars are around 15 years old, and while you might not look flashy, in a 15 year old Toyota or Honda, they are good cars with decent fuel economy, and you won’t regret buying them.

Don’t buy new, and don’t get a loan unless you must.

Renting vs Buying your House

Renting provides you with a zero maintenance arrangement with guaranteed expenditures (no surprises to wipe out your emergency funds) whereas a house provides you with a potential way to build your wealth, and usually (though not always) a better quality of life.

The single best way to save money is to live with someone else. If it is your parents and free, that is even better.

Insurance

Only carry it if you can’t stand the idea of not having it. Think: would it be catastrophic for my well-being or financial well-being if I didn’t have this and needed it?

i.e. If you have 4000 dollars in the bank, and a 6000 dollar car, then you should consider carrying comprehensive & collision coverage.

Life insurance only becomes crucial when you get to the having kids stage (then ONLY USE TERM INSURANCE not whole life) if that isn’t you, then don’t worry about it right now.

Rental insurance is often required by your landlord, and isn’t a bad idea if you are living in a high crime area, otherwise it’s probably not necessary.

Homeowner’s insurance: would it be catastrophic for your financial well-being if your house burned down? Yes. So buy insurance.

Pet insurance: This is would be a case by case scenario.

Health insurance: probably not crucial when you are single, young, and poor, but don’t go without for too long, since health issues can crop up (especially sports injuries or higher risk activities like skiing etc).

Picking Stocks

Is investing in individual stocks a good idea?

Let me change the question: can you make money on gambling?

Yes. But just because you can make money doing something doesn’t mean it is a good idea. The reward is always commensurate with risk. Big financial payoff = big financial risk.

Are you in a situation where you want to risk money that almost certainly you could get 9% annual returns on for the rest of your life in order to gamble? Maybe. Maybe. But don’t come crying to me if you don’t ever get your yacht.

Stock picking is horribly risky compared to dumping your money into a Vanguard investment fund like VTSAX and waiting for the returns to stack up. You are exposing yourself to massive downside risk, without diversification. (60+ stocks in various industries is where diversification benefits start to taper off).

There is no way to tell the future. Anyone who says differently is selling something. Every stock picking strategy that has ever been devised succeeded either based on luck, or failed in the long term compared to the buy and hold strategy.

I will state for the record that picking stocks can be fun. And it can be something that you talk about with your friends. If you must do it. Do it with a small percentage of your stocks.

Increase your earning Potential

This is the obvious but often overlooked way to increase your socioeconomic status. If you want to rise above your current status, you have to do it by increasing your earning potential. there are lots of ways to increase your earning potential: School, certificates, a willingness to stay late at work or a willingness to be the one to learn new things. Pick a strategy and knock it out, then pick the next one and knock it out.

Conclusion

I feel like I probably haven’t covered each of these in enough detail. In fact, I think each one of the headings above might deserve it’s own blog post. I’ll be back to cover them in the coming days, months, and years.

This chart is a fairly accurate view of my net worth over time, give or take a few thousand dollars. This is taken from my mint.com account(a personal finance tracking website). You may guess from the fact that I have data from the time I was ~19 years old on mint.com that I was a bit of a financial freak even at that age. You can see that my wife and I steadily saved money even during our college years(2009-2020). This is in spite of only making $26,555 collectively per year on average from 2012 to 2020. For perspective, the average wage in the United States for a single fast food worker is $25,848. This is about $13 an hour for a full time employee. Somehow we managed to save approximately 40% of our Gross income during that time.

How did we do it?

Eating Out Less

Alright, so prepare yourself for a new time consuming hobby. If you haven’t already guessed, it is cooking. I have been married to my wife for long enough at this point to realize that she loves cooking. I’m really fortunate that this is the case. But when I lived by myself, I never ate a single meal that I didn’t cook myself. Why? Well to be honest I wasn’t primarily thinking of the health benefits, though I did cook incredibly healthy meals. The real reason was that I didn’t feel I could afford to spend money on eating out. Why would I pay someone to wash my dishes, when I was getting paid ~minimum wage myself? I might as well do the extra hour or so of work each day to prepare all my meals (the meals themselves were not elaborate).

Which brings up another point. I’m not a picky eater. I don’t know what exactly sets our flavor palette, but I’ve noticed that I tend to be satisfied with my meal almost no matter what. It has to be pretty terrible for me not to enjoy it. Give me a bowl of rice and a bit of protein and I’m happy. This served me very well when I was cooking for myself, because I never truly developed a love of cooking, in part because I didn’t have quality cooking tools like pots, knives, or good stove. I was willing to compromise on taste because it wasn’t important to me, but if that is something that is important to you, I’m sure that you will be able to find a core set of recipes that will satisfy you and won’t let you down.

Give Less Gifts

It is hard for me to separate what is actually my preferences, vs preferences I developed because I’ve been a relatively low wage earner for so long. I just don’t love giving gifts. If that is your jam, and you love giving gifts, find ways to make your gifts more about the heart and the intent, and less about the dollar value of the gift that you give. You don’t need to buy your girlfriend a new laptop or camera in order to show them that you love them. They would probably be content with flowers and chocolates (my wife likes just flowers). Also, not to be a scrooge, but the American consumerist mindset around certain holidays and celebrations just doesn’t sit right with me. I recognize I might be on the fringes of society here, but people need to keep in mind that we live in such a wealthy place that extravagant gift giving has been normalized. I’ve seen people spend easily hundreds of dollars on their children. Right now I am getting my kids socks for Christmas, and helping their grandparents purchase a Tricycle for them. That is pretty much it for their Christmas gifts. It isn’t that I don’t love my children, it is just that I choose to let them know that in different ways that don’t require my house to be filled with crappy plastic toys that break after 6 days of usage.

Don’t be afraid to say NO to other people’s hobbies

So I admit, this one has always been a little more difficult for me to stick to. When someone invites you out to join them on some adventure that they like to take, it is hard to say no. But don’t ever compromise your goals just so you can spend more time with someone, no matter how cool they are. Some people’s hobbies are really expensive. My local ski mountain is $100+ for a single day lift ticket, and that wouldn’t even include a ski rental. I also have friends that spend thousands of dollars on their hobbies, and make a $120 ski pass look cheap.

Here is probably the most awkward of all the things that I’m going to tell you I do. I legitimately have said no to social invites if they include going to a restaurant. I know, I know, I’m a anti-social grouch, but hear me out. There is a group of people where I work that go out every Friday to get a meal together, during the course of which I’d estimate they spend about $25 each time, that is $1200+ a year in food that I’m not spending. Now perhaps I do eat $2 worth of food each Friday instead of going to the restaurant, but that still means I’m saving around $1100 a year on food. If I invest just this year’s savings, it will be worth around over $10,000 by the time I retire. I’d rather have the $10,000 than the extra time with my coworkers. Obviously this equation doesn’t work in every situation, and if I thought I needed to spend that money in order to advance my career for instance, I would totally do it.

The point is that you can’t let peer pressure force you to spend money that you otherwise wouldn’t spend.

Develop Cheap Hobbies

Cheap hobbies are things like hiking, camping, natural resource collection (I’m thinking of picking fruit, hunting, gardening, etc). To be clear though, your hobbies could be vastly different then mine are, the only requirement is that you aren’t spending more than about $5-10 a week on this hobby. (I’m estimating I spent something like that on gas money to do my hobbies.)

It isn’t only what your hobby is, sometimes it is how you do your hobby. Some people manage to spend thousands of dollars on something I can do for $100-200. Do they get 10x enjoyment out of it? Rhetorical question, the answer is no. They don’t. Also, if you find that you can’t participate in a hobby cheaply, maybe you should consider dropping the hobby.

Frequency of Epic Adventures

Don’t get me wrong. I think big expenditures to experience something that you will look back on for the rest of your life can be a great idea. A once in a lifetime expense may be worth it, especially if you can amortize the cost over your entire life. For example, a 3,000 dollar trip to Europe might be worth it, if you consider that it is only $1 a week when spread out over your entire life. Keep in mind that just because you have the money doesn’t mean you should use it for this. If $5-10 a week is your goal for your hobbies, just bear in mind that these large trips are coming out of the same financial bucket as your weekly hobbies are.

Develop Negative Cost Hobbies

Low cost or no cost hobbies are great, but they can’t compare to hobbies that make you money. Some of my hobbies are: buying and reselling anything, but particularly tools, trailers, and construction equipment. I’ve averaged somewhere near $2300 per year for the last 10 years. I’ve also kept up a hobby of doing construction work, particularly remodeling houses…I can’t take all the credit for this, but an older gentleman who I got to know during my time in Alaska saw potential in me, and asked me to renovate a house for him. We split the profit when it sold, and I made just a little more money on that transaction than I did on my full time job that year.

Part time work

If you are a full time student, you should be able to fit in some type of part time work in order to “start thy purse to fattening” This will do two things for you: first, it will provide you with additional funds. Second, it will increase your ability to be efficient with your time. If you don’t have time to waste, you will be less likely to waste your time. The goal is to fall into bed tired at the end of every day, not spend 1-2 hours every night catching up on the latest Netflix. If you aren’t doing school full time in the summers you are going to want to pick up a job. I decided to pursue construction full time in the summers since it was what I already knew how to do. Use whatever skill set you have to make money. If you have no skills you can always be a waiter, busboy, coffee shop barista, valet, janitor or window washer. Don’t let your lack of a resume stop you from being able to find ways to make money.

Dumpster Diving

Alright, this one is polarizing. I feel like about half the population hears me talk about this one and is like “I’ve always wanted to do that” and the other half of the population is like “you did WHAT?”.

Occasionally I run into someone else who has done this, and it always warms my heart to know I’m not the only one who hates to see “valuable” things go to waste. I put valuable in parenthesis because I’ve definitely brought home some things I shouldn’t have from time to time. Here is the thing about dumpster diving. If you are below a certain income threshold, say about $40,000 a year, I think it makes a lot of sense IF (a big if) you can find a dumpster that consistently tosses things that you can use or resell. For me, the only places that I’ve consistently found success was at Home Depot and Harbor Freight. Keep in mind that most of the time you will strike out when dumpster diving, but occasionally you will find something like this:

I managed to sell this chipper/shredder for $550. I spent about $40 and 30 minutes replacing the starter pull cord mechanism.

Chipper pulled from dumpster that I sold for $550

Be careful not to get injured while in the process of recovery (that chipper shredder weighed like 350lbs and I took it over the edge of a 9ft tall dumpster by myself…..that is a whole story in itself) there are other things to watch out for, like broken glass, sharp pieces of metal and used needles.

One more (often overlooked) spot to hunt is your local dump. I’ve lived in rural areas for most of my adult life, and when you go to the dump often there is no one around who cares if you dig something out of the dumpster.

Air Compressor from the local dump that I sold for $300

Obviously this money saving (or money making) strategy is outside the realm of socially accepted norms in some circles, but as long as you are safe about it and respect what people of authority say (store owners or dump employees) you’ll be fine.

Be flexible on living arrangements

During the first 3-4 years of our marriage we spent almost as much time living with people as living on our own. The first 9 months of my marriage I spent living in a rented room with my brother and his wife.

Next we spent 21 months in a section 8 apartment in Chicago, then we spent the next 10 months or so with a friend of my wife’s in a 2 bedroom apartment in Alaska. We haven’t lived with anyone else (except our kids) since then, but I would totally consider it if the opportunity arose.

Thrift Stores and Garage Sales

This might be self explanatory, but replacing the stores you currently shop at with garage sales and thrift stores will radically change the amounts of money you spend. I’ll confess that I’ve never been a fashionista, but I have a certain aesthetic that I find I can satisfy with regular stops at thrift stores and garage sales. Shopping isn’t my favorite activity in the world, but if I do shop, it is at thrift stores (for clothing) or garage sales (for other random things).

Only Buy what you NEED

If you want to become a financially responsible you must realize the difference between a need and a want. A need is something that you can’t do without. Food, shelter, and clothing are the ones that immediately jump to mind, but there are others. For example, if you live in the country where there is no public transportation, some form of transportation such as a car may become a need. Then you will need to carry insurance on it, pay for gas to operate it, as well as maintenance costs as they arise.

Don’t fall prey to the mistake of buying things you wouldn’t normally buy just because they are cheap. You didn’t save money there, you spent extra money.

There are three costs to every purchase: the cost to buy it, the cost to keep it, and the cost to maintain it. Having a cluttered house or garage is such a colossal waste of time. Sorting through supplies to find the one you need is expensive. Owning covered storage to put it under is expensive. Heating or cooling that area is expensive, etc etc etc.

Cool-off Periods for Big Purchases

Related to the “Wants vs Needs” concept is the idea of a cool off period. If you have something that you want to buy, but aren’t sure if it is a want or a need, or you know it is a want but you still are inclined to buy that thing, give yourself a cool off period. I’ve done cool off periods from 1 day to several months. It depends primarily on the size of the purchase. The idea is to let life go on for a while without that thing, and see how you manage. If you can manage for one month, could you manage for a year? If you can manage for a year, I guarantee you can manage for the rest of your life. Which means you should never buy it.

Don’t go to college

College is expensive. There is no way around that. I’m a huge fan of college as a way to increase your earning potential and job security, but I recognize it can be difficult to line up the free time and finances to go about pursuing a college degree. If you need help in this area, see my College On The Cheap post. Remember, college isn’t for everyone, but if you are trying to rise above your current socioeconomic status, it is one of the easiest ways.

Emergency Fund

If you don’t have an emergency fund, you are a ticking financial time bomb. Emergencies happen to everyone. Some common examples of emergencies might be:

• Job loss.

• Medical or dental emergency.

• Unexpected home repairs.

• Car troubles.

• Unplanned travel expenses. (death of a loved one etc)

The reason these can be detrimental to your financial health is that raising money to cover one of these expenses can become very expensive in itself. Short term loans, credit card debt, and other common forms of consumer debt tend to be a terrible waste of money. Once you paid off the original amount you needed to borrow, you still have to cover the expenses incurred by the lender in making that loan, aka you need to help them make a profit. If you do this, whatever benefit you received from not maintaining an emergency fund will be far outweighed by these costs. For the record, the following are not emergencies: 1. Expenses that you knew were coming. 2. Anything that involves a hobby of yours.

Roth IRA

Roth IRA’s allow you to be exposed to the upside of the stock market without tax implication. In other words, any gains you make on the money you put in a Roth IRA are not taxed. The reason I like Roth IRA’s for low income individuals is that you can use them as a form of bank account. 100% of your original contribution to a Roth IRA retirement account can be withdrawn at any time, for any reason, and without penalty. If you need to pull it out for any reason (for example to help your brother with medical bills) you can do so. I’ve contributed to a Roth IRA every year I when I was working full time and highly recommend you do the same.

Giving Back

As a Christian I personally find 10% to be a compelling minimum number to give back toward what God is doing in the world. If you ascribe to a different set of beliefs, don’t be afraid to support them. What you do with your money says a lot about who you are as a person. Don’t neglect giving unless you find that you cannot meet the basic needs as discussed under the heading “Only Buy what you NEED” above.

Budgeting

Some of you may be disappointed to hear this, but I’ve never found budgeting to be a compelling or important part of my financial journey. Maybe I’m just so cheap that things like budgets don’t help me. Maybe I’m just too lazy to budget. I don’t know, but I always have good idea of how much money is coming in due to monitoring my bank accounts, and I always know where my money is going from my credit card statements. I find that is enough to set me on the right financial path. If you disagree with me, that’s fine. Go find another blog to read… haha.

Self Discipline

My single most important piece of advice: do whatever you can to increase your self discipline. This is the one life skill that will take you further than any other in life. Don’t let money control you… control your money.

This post is getting long, so I’m going to stop it here and make another post with the same title.

The average American Family spends $237 a month on subscriptions. Here are my strategies for avoiding these income sucking recurring expenses:

Music Streaming Via PC:

Youtube works great for this if you want specific songs. If you are looking for a good playlist mix, then Pandora is worth a try. Many of the bands that I listen to were discovered through songs from Pandora. See my adblock section to avoid listening to sponsorship ads on both Youtube and Pandora.

Music Streaming Via Phone:

I find that this isn’t a terribly important thing for me. It isn’t that I don’t like to vibe, but I tend to spend a lot of time driving in the car by myself at this period of my life, and I have always found that time conducive to audiobooks. If I do want to listen to music, I have an app called NewPipe, and this allows me to listen to youtube videos ad free. It is a great app, and has totally replaced the youtube app on my phone.

Adblock

I use the uBlock Origin extension for Firefox on my laptop. This blocks commercials on Youtube and Pandora. On my phone I use the extension “NewPipe” when I play youtube videos. This eliminates sponsorship ads. I don’t listen to Pandora on my computer.

Amazon:

I use Ebay and Aliexpress extensively. That being said, Amazon is the one subscription that I pay for. I have a student account, which is half price. In 2023, I spent about $6000 on Amazon.com. Which means that my Amazon Prime Visa credit card (which nets me 5% back per purchase instead of the 2% that I get with my regular cash back card) netted me around $300, which is $180 MORE than a 2% cash back card would have. Thus paying for my subscription, and making me a tidy profit. Additionally, and I can’t say this for certain, but I suspect that the customer service representatives are more accommodating when they see that I’ve had a subscription for 9 years or whatever. On any given year I save ~3x what I pay in subscription costs. Most of this is through product support. For example, recently (last week at the time of my writing this) I received a refund on a $200 item that had a few pieces missing. I was able to order the missing pieces for about $30 online, meaning that that single transaction paid for the next 3 years of my Amazon membership. I also provide one of my siblings and my parents access to Amazon, since they are also cost conscious value added shoppers like me.

Netflix/Amazon Prime/ Streaming Platforms

First of all I discovered a few years back that no one really cares if you’ve watched such and such a movie or series. People often like to relate to others through film, and they will bring up plot lines or movie quotes, and if you don’t tell them differently, they’ll assume you have some idea what they are talking about. I personally enjoy reading synopses of shows or movies on Wikipedia, and occasionally I’ll watch a few movie trailers on youtube. This gives me the basic familiarity with the plot lines, characters, and funny moments without the massive time investment required to watch the whole movie or tv series. People, for whatever strange reason, like to be able to connect over something that they have both experienced. I like to be able to relate to people, and I don’t follow sports (another common connection point), so I try to spend an hour or two every few months doing this instead.

Personal Fitness:

When I was in college and had access to a gym, I used it 2-3 times a week. I found it to be helpful to have someplace where I could go, not think about anything, and just do some physical activity. Regular exercise at home is difficult as I have young children who like to be with dad and copy whatever he is doing, and it just makes blocking out time and space to work out challenging. Right now I am building a house, and I find that the amount of exercise that I get from moving raw materials around and crawling on and off my tractor provides sufficient exercise for me. I honestly think that I may be more fit now then when I was hitting the gym multiple times a week while in college simply because my weekends are very physically demanding. As time goes on and I finish the house build (and gain a bit of free time) I’m open to the idea of a gym membership, since if it takes me from zero exercise to multiple days of exercise weekly, the price of the gym membership would be insignificant in comparison to health care expenses down the road.

Phone Plans

For years I was on a family plan with my brother on AT&T. I felt like my connectivity was good with them, but they were $30 a month per phone. Not as expensive as some people’s plans, but I eventually found something better. I now spend 12-15$ a month on my phone plan with RedPocket. I have the same network (AT&T) and I’ve never really noticed any significant connectivity issues.

News and Magazines

Do people really still spend money on this? I use my local library’s subscription if I ever need to log on to the New York Times or a similar website to finish an article, but mostly I’ve come to the realization that it isn’t important to keep up on the news. Anything that is truly important tends to get communicated to me via my friend group, and that is, in my opinion, a much better way to learn about news then any journalist, no matter their style. This is because news doesn’t matter. 99% of the news article I’ve ever read didn’t truly matter to me. If this is your hobby, that is fine, but it certainly isn’t mine. I can’t find it in me to care.

Food and Meal Services

I think it is important to carefully structure your life to allow time for the cooking and consumption of food. I’ll be up front and say my wife does significantly more of the food prep than me. I tend to be on tap for waffles, pancakes, and scrambled eggs, etc. She seems to enjoy it, and I’ve never felt the need to step in and take it from her, though if she ever goes back for her Master’s there is a good chance I’ll need to step it up.

Gaming:

People often talk about hobbies as something that they couldn’t imagine themselves without. Video games used to be that for me. I loved them. I still do, there are about 3 or 4 strategy games that I’ve played over time that I would love to spend an afternoon (or seven) enjoying. But I have instead chosen as my hobbies things that are more physically demanding. Hiking, construction, etc. Choosing not to game was a default because I wanted to do things with my time that prevented me from gaming (construction/hiking/electrical engineering). If I had continued gaming instead of taking up those hobbies, my career prospects, financial situation, and probably my mental health would have all suffered.

Software and Cloud Services:

So I do pay for this website, it is about $75-100 annually. That is only because I want a public platform where I can share who I am (and my thoughts) without pointing someone to a social network website. I don’t pay for anything else software or cloud related. I’ve used Libreoffice for years (though my work and my school both currently have a Office 365 subscription for me).

Financial Services

I do pay fees on several of my accounts, but they aren’t management fees, just fund fees of around 0.08%. My bank(s) charge me nothing. I do have a loan for the property that my wife and I recently purchased to build our house on, so I spend money on the interest on that money, but the amount I spend on interest is less than the appreciation on my property right now, so I’m not too distraught about it.

Book and Audiobook Services:

I use my library extensively for this purpose. Overdrive, Hulu, and the free website Librivox. It is rare that I can’t find a specific book, If I do, I just add it to a list, and check a few years later to see if it’s distribution has broadened. Very rarely do the books I read need to be finished by a certain date.

The investing strategy that I follow is a “get rich slowly” scheme. I’m not into chasing down returns. I don’t need high risk/high reward for the majority of my investments. If you don’t want to spend your life consumed by what the stock market is doing, keep reading. If you feel like that is something you need, I recommend pulling out 5% of your portfolio and doing day trading or cryptos or whatever you need to do to get that out of your system, because emotion based investing is the enemy of your portfolio. I understand that for some people there is relational component; that picking stocks or sharing in current trends may allow you to participate in conversations with your friends. I don’t discount that, but if you want the best returns on average, with significantly lower risk overall, don’t do that with your main portfolio.

I could have titled this post “Investing Strategies for Boring People”, but you probably wouldn’t have clicked on that one would you? If you like high risk activities, and want your money to make a huge gains, find another website. What I’m espousing here will change your life, and leave you with a near 100% certainty of adequate nest egg upon retirement, but it won’t double your initial investment in 6 months. That kind of growth is unsustainable, and certain to reverse at some point. The risk is commensurate with the reward.

Some people hear the term “Passive Investment” and think bad returns. That is simply not the case. I like investing in the entire stock market. The real return of the market is 8.8 percent since 1887 (that is without the negative annual return of 2% from inflation, so actual rate would be 6.8%). That is a rate of return that would allow you to retire comfortably on just 6k per year investment throughout your working life.

Passive investment should be part of your investment strategy, if you get the itch to actively invest (I accept that people like to gambling with their money for fun) it is highly expedient for your long term wealth building that you only do so with a small part of your portfolio. The risk from this method is that you may not even get the baseline of the total stock market’s annual increase, additionally, you are likely exposing yourself to several times the amount of risk, so your risk adjusted return was even lower! Risk is one of the most underestimated factors in any investment strategy. When you invest in a high risk sector, you basically become your own insurance. If a catastrophic event occurs, you are the one who pays out, if no catastrophic event occurs, you make money, and good money at that! Ever read the “Black Swan” by Nassim Taleb? There are always unforeseen catastrophic negative events that will occur. So beware.

I’ve noticed that whenever stocks are going up more rapidly then normal, the stock market tends to a get a lot of additional press attention, and this often draws inexperienced investors into the market at the worst possible time to enter the market. When the market corrects there is a lot of negative press, and inexperienced investors may be influenced by these reports to get out of the market. Fight that urge.

This is what happens when you try to beat the market average. People trying to beat the market find themselves on the losing side just as often as the winning side, but they pay a higher price. The fees of an actively managed account often eat up the profit that the account claims to deliver. In addition to this, the tax implications from all the trades necessary in an actively managed account make it a particularly poor choice for non-tax advantaged accounts. It is estimated that the global financial services market is 26.5 Trillion dollars. That’s Trillion with a T. 20-25% of the world economy. Someone is making money off of every dollar you save, invest, transfer, or send. It is in their best interest to convince you to pursue an actively managed account.

One of the largest indicators for the success of a fund is the expense ratio, it is pretty much the only thing that you know ahead of time when you buy into a fund. In the field of investing, it is a generally accepted maxim that “past performance is no guarantee of future results”.

Time to get practical:

The best place that you can dump your money if you want a “set it and forget it” approach to investing is a target retirement date fund from Vanguard such as VFFVX.

I’m a huge fan of Vanguard. They are non-profit, which allows them to have low fees on most/all of their mutual fund offerings, the funds I’ve used are:

VTSAX Total Stock Market Index

VTIAX Total International Stock Market Index

VFFVX or any other Target retirement date fund

Fidelity has some zero fee funds covering the U.S. and international stock markets. The funds are: FZROX and FZILX, and if I was just starting out and around 20-25, I’d consider dumping half in each.

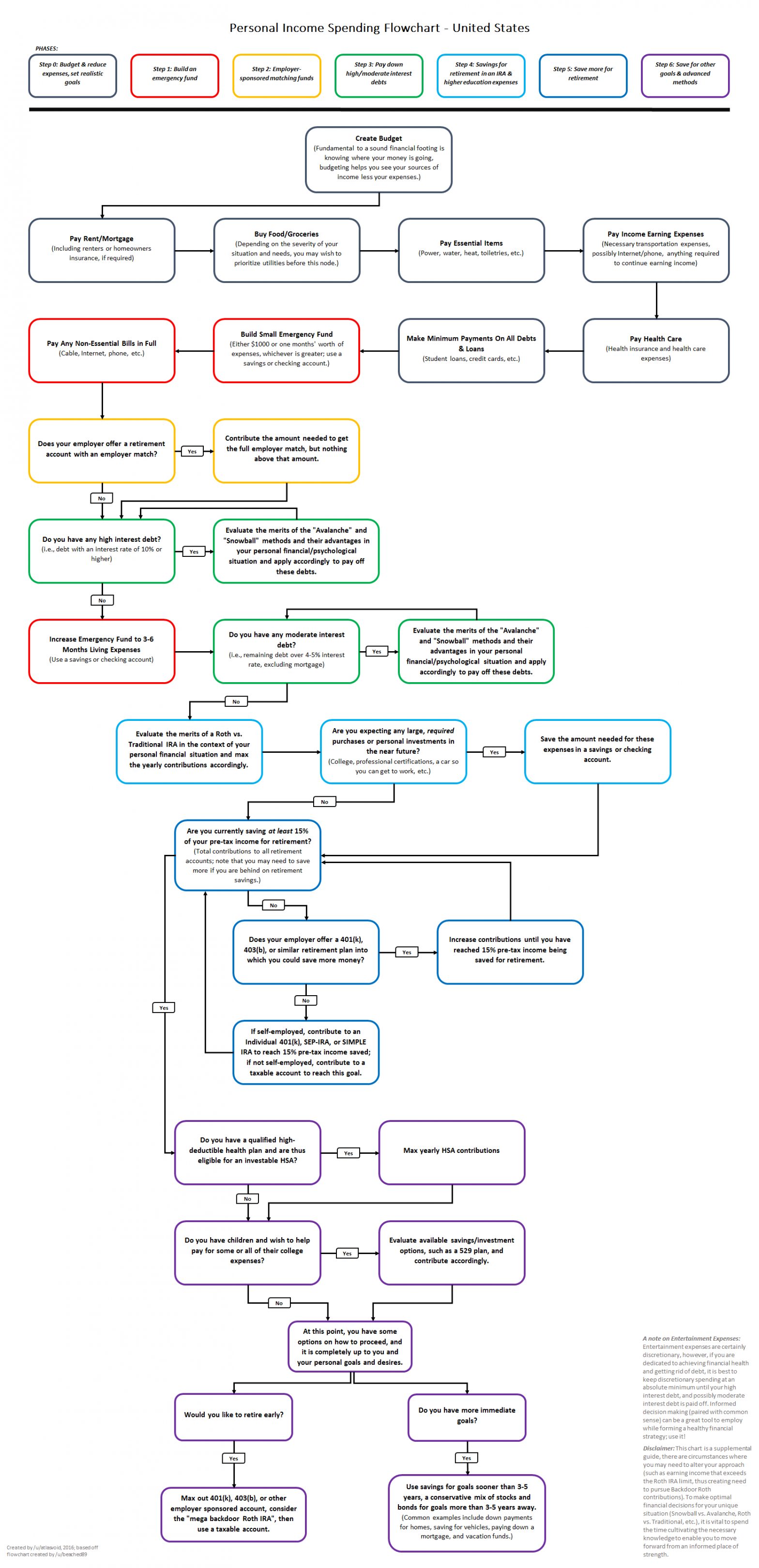

Please take the time to read the common topics section from Reddit’s “Personal Finance” website. That resource will give you a great overview of investing and personal finance. The graphical flowchart is an especially great resource.

I do not recommend investing if your timeline is less than 5 years (as would be the case if you were planning to pay off student debt with the money/put a down payment on a house/buy a car). In that case you’d want to consider a high interest Savings account or similar.

This will require you thinking ahead. It takes some serious planning in order to figure out what your future holds and what you will want to do with the money. Don’t hear me wrong, I think you should invest a percentage of every single paycheck that you earn over your career, but don’t plan to take any of that invested money out to finance a particular purchase in the near future.

There are other ways to invest intelligently besides the stock market. The ones that come to mind are Real Estate, Business Debt, and personal improvement(usually education). Please see my other articles on these subjects.

Don’t chase past earnings in mutual funds, and don’t pick stocks. You will not win in the long term. Everyone likes to remember (or brag about) that one pick from years ago that turned into an Amazon, but think of how many companies didn’t make it through the dot-com crash. Thousands… are you going to pick the stock that goes to the top? Unlikely. If there is any doubt about this point, I can forward you some literature so that you can convince yourself it is a bad idea to play with this. It is also a royal time-suck. Devote your time to getting better at your job or developing a sidehustle, not this.

If firecalc doesn’t change your life, nothing will. It takes a minute to figure out how to use it, but it is fun to see what your investment will grow into if you let it.

https://www.citi.com/credit-cards/credit-card-details/citi.action?ID=citi-secured-credit-card For those who are just starting their financial journey with no credit history, I recommend a secured card because most likely you will be turned down for anything else. Having a credit score is important because it allows you to use credit cards with rewards. (My credit card (Citi Double Cash) gives me 2% back on all purchases). It is also important if you decide to purchase a house anytime in the next 10 years or so. If you get turned down by one bank for a secured card, apply for another, and keep applying until someone is willing to take a chance on you. I walked into a US Bank at the age of 19, and was turned down by their system, but the banker called me a couple days later and said he was willing to take a chance on me. They made the right choice, as I’ve continuously maintained an account with them since then, and have yet to make a single late payment.

I recommend storing any savings that you will not be using in the next 4 months in this bank account: https://www.ally.com/?context=bank This bank gives you one of the higher % interest return per year for using them, as compared to 0.1% as an average for all banks in the US. This is important because it gives you a decent return with no effort on your part. It is dead simple to transfer money to and from your local bank’s checking account (or credit union) directly from this account. It literally takes 3 button clicks once you log in to transfer money either direction (And takes 1 business day).

For a retirement investment account, I recommend Vanguard: https://investor.vanguard.com/ira/iras Create a Roth IRA and contribute up to $6000 (Your spouse or significant other can also contribute this much). This is taxed money, but it is not taxed when you pull it out at retirement, and you can also pull out what you put in at any time and with no penalties or fees. The fund that you will buy is a “Target Retirement Date fund” for year ~when you will retire. This manages your funds for you so you never have to think about it. If you want to invest more than this, or in other things, you can, but I’d recommend this at a minimum every year you are working.

“Investors should remember that excitement and expenses are their enemies. And if they insist on trying to time their participation in equities, they should try to be fearful when others are greedy and greedy only when others are fearful.” — Warren Buffett

There is money to be made on the meteoric rise of cryptocurrencies, just watch out that you don’t lose it all on the way back down. Like every bubble, there will be winners and there will be losers.

Like any investment strategy, the potential reward for investment must balance out the risk. At this stage, Cryptocurrencies are both risky and (potentially) very rewarding. Anytime there is “easy money” to be made, there is going to be an eventual collapse, because when the people that flocked to an investment due to a sharp increase in price experience their first dramatic decrease in price, they won’t enjoy it, and will pull out of the market, or switch to another investing medium. “But,” you exclaim “retail investors only account for 20% of the market!”. That is indeed true, but there are two things you need to remember:

It doesn’t take 100% of people getting out of the market for the price to drop drastically, it only takes people being unwilling to buy at the current price. If nobody is buying, then the people who want to get out the market will force the prices down rapidly.

Institutional investors have fiduciary responsibility to protect their current investments. That means when the market is going down, they may pull money out out to protect their investments, which forces the market further south.

You probably wouldn’t have guessed it, but I’m actually very bullish on the role that cryptocurrencies will play in the future of mankind. What I’m not bullish about is any particular cryptocurrency. Do you remember the dot-com bust? Remember pets.com? No? It lasted 9 months after it’s IPO. I’m not saying that cryptocurrencies are stocks, they aren’t. What I’m saying is that survival of the fittest dictates that many die out before we find who will provide long term value to users, and eventually long term gain to investors.

I entered the cryptocurrency world with money that would have otherwise been left sitting in a bank account in late 2017. I didn’t bet big, because I was a poor college student. But I did it right, I had a well diversified portfolio of over 40 “alt-coins”. I realized at some point that the current market trajectory was unsustainable, (January 15th of 2018) and took my money out. For those who are wondering what happened in the market, the following 3 months were an absolute blood bath, it tanked, and tanked hard. I only took out what I had put in. I liked to pretend that the rest was “monopoly money” but in reality I still wanted to bet on the crypto currency market. In all I’ve roughly quintupled my initial investment. Am I happy about that? I guess I am, but I can’t help thinking that it was mostly luck. I had no idea what direction the market was going to go, and I had no idea when I needed to pull out of the market, I had no idea that if I left my money in there that the market would eventually come roaring back. I have a lot of friends that jumped in during that time, lost a bunch of money, sold out, and never got any of it back.

I learned a few different things about cryptocurrencies:

They are volatile. Use this to your advantage. Don’t be afraid to realize gains.

They are unpredictable. Don’t allow yourself to get emotionally involved in the current market direction. This will cloud your choices. Just because the cryptocurrency market at large or one individual cryptocurrency is currently killing it, doesn’t mean that can’t reverse today and never recover.

There is no intrinsic value for cryptocurrency, they are simply worth whatever people are willing to agree to pay for them. This means that if someone discovers a bug within cryptocurrency code that can be exploited, the value of that cryptocurrency drops fast, potentially even to zero.

Exchanges can be hacked. I personally lost a small portion (8%?) of my investments to the “Cryptopia” hack.

The cryptocurrency market is unregulated. Sketchy stuff happens in unregulated marketplaces. The pump and dump groups are a great example of this. Insider trading is rampant. It isn’t a good enough reason for me to pull my money out, because I’m in it for the long haul.

Physical crypto-currency wallets are annoying. The more coins you have, the more annoying they are. Even the slickest and most well put-together wallet is annoying to use. If you don’t want your coins to be at risk of hacking, you’ll need to manage that physical device. And be aware that there is a very real risk of loss of that device or it’s passcode.

Bitcoin, although a favorite amongst those in the cryptocurrency world, holds no chance at long term supremacy. The energy usage of Bitcoin currently stands at about 0.5% of global usage. That is a massive amount of wasted energy, and a bad sign for bitcoin itself.

To date, I’ve although I’ve had many enthusiastic conversations about the technology behind cryptocurrencies, I have not yet counseled someone to buy, and I always tell people to sell. Don’t get me wrong, I’m bullish on the crypto-market in the long term, but I’m not bullish on the average individual being able to pick the winning cryptocurrency. So if you feel some urge to gamble 5% of your investment portfolio on something with serious upside….sure, go for the broad crypto market. Otherwise, stay far away.

For those who are interested in some further reading, allow me to point you to the following link… I’ll warn you that although there are plenty of coherent thoughts in this article on the crypto space, I don’t agree with him that there are zero potential use cases for Crypto, simply that the exuberance seen right now in the crypto market is severely misplaced and is in essence a massive bubble. I especially appreciate what he has to say about NFTs. https://www.currentaffairs.org/2022/05/why-this-computer-scientist-says-all-cryptocurrency-should-die-in-a-fire/

Listen, if you want to slip the colleges an extra $10,000 a year for your college experience, I’m fine with that. I’ve come to peace with the fact that not everyone can do what I did. But a quality education is still available to people at an affordable price if they know where to look. Anyone can graduate from college debt free if they want to. And that means you… yes, you! If you want the story version with all the juicy details, keep reading. If you just want the strategy I used, skip to the section with the headings.

Here is how I went about getting not one, but two undergraduate degrees for what many people spend on their first year (or even first semester!) of undergrad, and how you can do the same. Some of these tricks I used from the very beginning, and some I learned several years in.

There are 5 schools in my college experience, I’ll start with the most recent first:

I attended a state school in Alaska. The average cost of attendance was $4400 a semester, which is far below average, even for a state school. On average I paid less than $2200 a semester. The difference was made up by scholarships. My overall cost could have been far less, but I didn’t decide to attend school my first year until after the deadline for scholarships had passed. In other words, 56% of what I spent at the University of Alaska was during my first 12 months there. Total cost for 4 years of full time school? $17,600

I averaged $1000 dollars a semester for 3/4 of this undergraduate degree. How? Part of it is luck; I received in-state tuition at one of the cheapest state schools in the USA. The other part of it was hard work. I spent time on local scholarships, and they drastically reduced my overall school cost. In fact, I treated scholarship applications as a type of part time work. During the time when most scholarships had their deadline, I worked non-stop on them. Probably averaging 5 hours per scholarship application. At this point I already had a bachelor’s degree in education and this worked to my advantage as I filled out scholarships. I spent far less time than some people on scholarships, and I turned out high quality (judging by my success rate) applications.

I went to two different schools where the tuition was free. Yes, free. They were Christian schools and their goal, aside from education, was to prevent their students from graduating with debt. That didn’t stop one of them from charging ~$1000 a semester in fees, but who am I to complain? This is probably of limited usefulness to most you, since not everyone wants to go to a Moody Bible Institute. But it was great for me, and I walked away at the end of 4 years with an accredited undergraduate degree in education (Counseling to be precise).

After starting at this school, I learned about another school that would accept my credits toward an accredited bachelor’s degree. That sounded like a miracle to me, since I had no idea that accrediting agencies existed just a few months earlier, and hadn’t thought to check my school before I began. So began my process of transferring credits from one school to another. I’ve now attended 5 different schools. I promise that I hated school when I left highschool. There was nothing that sounded more boring. Learning grows on you though.

The strategies that I employed:

FASFA (Free Application for Federal Student Aid)

If you haven’t applied for this, you are throwing away money. Every single person who goes to school needs to apply for the Fasfa. Try to apply about 9 months before your classes start. At one school I went to I received a “Pell grant” for 110% of my tuition costs. This covered my tuition and all of my books, and I had some spending money left over. I can’t emphasize how important this is, especially if your parents are low income (student aid awards consider the income of your parents, as well as your own, until you turn 24, when it becomes dependent on your income alone).

This is the website where you’ll need to go to fill out the forms:

If you can, find some people that you respect to rent with. This could go really well, or it could be really hard. Even under the best circumstances, I’ve never lived with a group of people without having some high stress moments, but it has always been worth it. You will get to know people very well when you live with them, so make sure they are worth your time before you move in with them. I lived on campus, or off campus in a house with others up until I moved in with my wife.

Part time work

I highly recommend part time work to most people, unless they are shooting for a 4.0 GPA or have some other good reason to not work. I highly recommend looking for a part time job during your freshman and sophomore years in school that will allow you to work on homework while on the clock. Once you are a junior or senior, you hopefully be able to find a position that will build skills for your career. During each of my 4 year degrees, I graduated with more money in the bank than I started with. In order to do this, I worked full time in the summers doing what I knew how to do, construction. Use whatever skillset you have to make money. If you have no skills you can always be a waiter, busboy, coffee shop barista, valet, janitor or window washer.

Loans

Some people seem to have an allergic reaction to loans. They break out in hives at just the mention of that dreaded word. Maybe you are this type of person, you wake up clutching the sheets and shouting “24% APR COMPOUNDED DAILY, NOOOOOO!! Please read this paragraph with great care, because I’m going to tell you a secret that can change your life. Debt is only bad when it decreases your overall financial well-being. To illustrate this, take home ownership. Historically speaking, home ownership can be a great investment. If real estate prices rise at a greater pace on average then the current going interest on a mortgage, you may make money by being in debt! I bring this example up first, because the debt averse person is usually willing to make an exception for a house, simply because most people can’t afford a house without taking on debt. College “CAN” be far more advantageous then any mortgage, even with deep debt. Consider this: with 4 years of school, I literally doubled my earning potential. I have pay stubs to prove it. Even if I had to go into debt to do school (which I didn’t), it would have been a brilliant strategy. Say for the sake of argument that I needed to take out loans to finish that degree. The average student loan at graduation is $25,921. That means I could have paid my loan back in the first year after graduation, and still had an extra $10,000 to spare, not to mention a lifetime of increased earning above that. Do you understand why I think some loans are an acceptable risk? The risk is actually quite low for academically competent individuals who carefully research their desired career path and understand how the specific degree program and school that they’ve chosen will affect their work life & post graduation finances. If that isn’t you, then you need to do the research. If you are the type of person who isn’t capable of doing that sort of research, then maybe college isn’t for you.

Textbooks

I have an overactive conscience that won’t allow me to use any digital content that I don’t personally own, which eliminated the common strategy of finding textbooks online. What I did do was buy a previous version of the textbook, and often literally paid $200 less than my classmates for the book. Then I’d borrow someone’s book and copy down the questions that the professor required for that week, using my own book for everything else. I’d estimate this can save you from $150 to $800 per year on the cost of books. Libraries sometimes carry class textbooks, but you’ll have to email the professor early in order to find out what book the class uses, and check it out early from the library to be sure you get a copy (there are other cheap people out there too).

Transportation

If you don’t have to have a car, don’t have a car. Insurance, gas, and maintenance can really add up, especially if you can’t do maintenance yourself.

Standardized Testing:

Incidentally, I have never taken the SAT or the ACT. I started my college career at a non-accredited school which didn’t require any standardized test before entrance, and after that I was always a transfer student. But I have done my fair share of other standardized testing. Mostly college placement exams and CLEP tests. I did 17 CLEP credits. If I had been able to do more for my degree programs, I would have. They were so much easier then taking a class. The average time that I studied for my CLEP tests was about 8-10 hours. Less than many final projects, even for easy classes. I never failed a CLEP test, so I probably could have studied less. The one exception to this was Chemistry. I studied Chemistry for hours and hours. I never took Chemistry in highschool, so it was some kind of miracle that I was able to pass a CLEP test that covered two semesters of college level chemistry and lab. I highly recommend CLEP testing as an advantageous way to knock out some credits for (virtually) free. I think the tests were $80 each, including the proctoring fee. College credits are on average about $500, which means you could be saving thousands of dollars by taking CLEP tests. If you have interest in getting a college degree using CLEP tests or similar strategies check out www.degreeforum.net.

Scholarships:

I already mentioned it above, but spend time on scholarships. I don’t know how to emphasize this any more strongly. There are scholarships for people with good grades, but there are sometimes even ones specifically for people with bad grades. I recommend spending the most time on regional or local scholarships, then state scholarships, then national scholarships, as I never received funding from any national scholarships, but plenty of help from the others. Call the school you are attending, speak to their financial aid, and ask about scholarships that you can sign up for. They will steer you in the right direction. It is even worth setting up an appointment with someone who would know about scholarships if possible. Do this long in advance of the start of the school semester. My school had a cutoff in February for most scholarship applications for the following fall.

Know How Hard Your Classes Will Be

I highly recommend looking up every professor that you take using this website:

It gives you some idea of how difficult the professor will be. This allows you to plan much better for what classes to take in any given semester before the semester starts. This is only useful if other people have put a fair amount of reviews up. If you have a friend who is a year or two ahead of you in the program they will likely have a much better idea of what courses & professors will be difficult or easy.

Technical Schools: “Tech School”

These are public colleges that focus on non-four year degrees. They are cheaper, and usually require lighter homework requirements per credit hour. I knew people who couldn’t pass the physics or chemistry classes at the 4 year college, and they reported significantly easier classes at the tech school. They can also be a good strategy if you want to go to college, but haven’t decided on a major yet.

American Opportunity Tax Credit

I’ll just include a link so you can look it up yourself, but America subsidizes virtually every American college student with this tax credit.

Transferring credits is hard. It is so time consuming to try to figure out what credits will apply where. You will likely spend HOURS trying to understand how your credits transfer from one school to another.Take the time. It is worth it. I remember spending literally days figuring out what credits would transfer to my next program in school.

Honestly the credit transfer system for schools is broken. At some point you will need to see an academic advisor to see if your credits will transfer in. Very few schools will analyze your transfer credits unless you are an admitted student. If you are transferring credits, apply to the school and see what they say. If you don’t get the transfer credits you need, you are might lose out on your application fee, but that is better than having to retake entire classes because the school wouldn’t accept your transfer credit.

Once I started school, each progressive school accepted transfer credits from the school before it. It is a bit of a hassle to transfer as they usually require you to provide all kinds of information about the course work from your prior school, but think about how much time (and money) you’ll save by not having to complete any additional coursework! Transferring credits is a great strategy and you shouldn’t be scared to do it!